Federal Budget Summary 2026

A summary of the Budget changes that could affect your financial plans.

Federal Treasurer Jim Chalmers has handed down the 2026–27 Budget, with a strong focus on housing affordability, tax changes and cost-of-living pressure. This article addresses key announcements and highlights why it may be worth reviewing your financial position.

Overview

The Budget comes at a time of higher living costs, inflation pressure and slower economic growth. The Government says this Budget is designed to help address this by making the system fairer, especially for younger Australians trying to enter the housing market. To do that, it has broken election promises and proposed significant changes to negative gearing, capital gains tax and the tax treatment of discretionary trusts, along with a range of broader economic measures.

Some of these changes are among the biggest investment tax reforms seen in many years. While the measures are intended to support first home buyers and encourage more new housing, they will change the way investors think about investment options and whether to hold assets personally, through a trust, or inside super.

It is also important to remember that many of these changes are proposed for future years, include exceptions, and may still be refined before becoming law. Consequently, while the headlines are important, the real question is how any final rules may apply to your personal situation.

That is why financial advice is very important. Even when a Budget measure sounds straightforward, the impact can be very different depending on your personal circumstances and future goals.

Property and investment changes

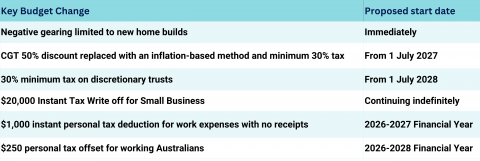

One of the biggest announcements is the proposed change to negative gearing and capital gains tax. From 1 July 2027, negative gearing for residential property is expected to be limited to new builds. Existing properties held at Budget night are expected to keep their current treatment. If an investor buys an established property after Budget night, losses may still be offset against rental income and carried forward but cannot be offset against salary or wages.

Capital gains tax changes

At the moment, investors generally receive a 50% discount on capital gains when they sell an asset they have held for more than 12 months. Under the Budget proposal, that discount would be replaced from 1 July 2027 with a method that adjusts the cost base for inflation, along with applying a 30% minimum tax on net capital gains. These changes are proposed to apply to all investments including previously CGT exempt pre 1985 assets.

Transitional arrangements for capital gains tax changes

The proposed transitional arrangements are very important to note, apply to eligible CGT assets other than new residential properties and are proposed to be:

No change in arrangements for assets purchased and sold prior to 1 July 2027

Assets purchased on or after 1 July 2027 will be treated wholly under the new arrangements.

Assets owned prior to 1 July 2027 and sold on or after 1 July 2027 will be treated under current arrangements on gains made prior to 1 July 2027, and under the new arrangements for gains made on or after 1 July 2027 (with no impact until gains are realised).

The 50% CGT discount will apply to the difference between the asset’s cost base and its value at 1 July 2027.

Indexation and the minimum tax will be used to calculate the CGT on gains accruing from 1 July 2027 (using the asset’s value at 1 July 2027 as the asset’s cost base).

An asset’s value at 1 July 2027 will be determined by taxpayers as part of their tax return in the year the asset is realised.

Taxpayers can either:

seek a valuation of the asset as at 1 July 2027, which will include using quoted prices for assets such as listed shares; or

use a specified apportionment formula that estimates the asset’s value on 1 July 2027, based on its growth rate over the asset’s holding period. The ATO will provide tools to estimate this value for taxpayers.

Changes for family trusts

Another significant proposal is the introduction of a 30% minimum tax on discretionary trusts from 1 July 2028, aligning their treatment more closely with company tax. In broad terms, this is likely to impact current planning strategies that might have produced a lower tax outcome.

Not every trust will be affected, Fixed Trusts and some kinds of income are expected to be excluded, and restructuring relief may be available for certain people who want to move out of a discretionary trust structure. If you use a family trust or business trust, this is an area worth reviewing carefully with your adviser and accountant.

Superannuation and SMSFs

One of the more reassuring parts of the Budget is that superannuation, including self-managed super funds, at this stage has been left out of the proposed capital gains tax changes. In other words, the current capital gains tax treatment inside super is expected to stay the same for now.

Personal Income Tax

Approximately 6.2 million Australians will be able to claim a $1,000 instant tax deduction for work expenses without receipts from the 2026–2027 financial year, and separately receive a $250 working Australians tax offset from the 2027-2028 financial year.

Productivity and small business support

The Budget includes a suite of measures aimed at lifting productivity. The current temporary $20,000 instant asset write‑off will be made permanent for businesses with a turnover below $10 million, allowing the immediate tax deduction of eligible asset purchases. Small businesses will also gain access to an additional two‑year tax loss carry‑back period, enabling current losses to be offset against taxable profits from the previous two years.

The Government will increase the expenditure cap for the Research and Development tax incentive and separately, the Budget includes a productivity package designed to reduce regulatory compliance costs for businesses by up to $10.2 billion per year.

Summary of key proposed changes and timing

Make it stand out

Conclusion

This Budget may lead many Australians to take a fresh look at how they invest, how they hold assets and how they plan for their future.

While some changes may not begin for some time and of course, there are still significant details to be refined and they may change as the legislation is finalised, it is important to start to prepare before the changes become effective. It is particularly important to be aware of the valuation of assets at 1 July 2027 in regard to the calculation of future CGT on sale of assets.

Financial advice can help you understand what these proposals may mean for you, avoid knee-jerk decisions, and make sure your strategy still suits your goals. What works well for one person may not be right for another. As part of their regular review of your financial plans, we can help you to understand how the 2026–27 Federal Budget could affect your financial position.

Have more questions? Reach out to our knowledgeable team today.

General Advice Warning

The information in this presentation contains general advice only, that is, advice which does not take into account your needs, objectives or financial situation. You need to consider the appropriateness of that general advice in light of your personal circumstances before acting on the advice. You should obtain and consider the Product Disclosure Statement for any product discussed before making a decision to acquire that product. You should obtain financial advice that addresses your specific needs and situation before making investment decisions. While every care has been taken in the preparation of this information, Infocus Securities Australia Pty Ltd (Infocus) does not guarantee the accuracy or completeness of the information. Infocus does not guarantee any particular outcome or future performance. Infocus is a registered tax (financial) adviser. Any tax advice in this presentation is incidental to the financial advice in it. Taxation information is based on our interpretation of the relevant laws as at 1 July 2020. You should seek specialist advice from a tax professional to confirm the impact of this advice on your overall tax position. Any case studies included are hypothetical, for illustration purposes only and are not based on actual returns.